I ended my last update with an examination of the abnormally warm February weather we had, and what it meant for production. It subsequently got cold and snowy – the picture here shows dad’s truck and trailer jackknifed with an 800-gallon load of sap on it during the start of the second of three Nor’easters. We had to dump 400 gallons to get the truck straightened out, and only then with help from the town sand truck. Good times had by all.

On March 1 there was no snow in any of our woods. As I write this, the snow in the Hall bush is closer to my waist than my knee. The snow and cold have pretty much brought production to a halt, though we boiled twice as snow piled up on the sugarhouse roof. The falling snow – the way it made everything so quiet – and the lack of urgency were both lovely. It felt old school in the best way – a throwback to grandpop’s farm and the old flatpan aboil beneath a simple shed roof; large, wet snowflakes like moths before a hissing Coleman lantern; three generations of family gathered before the sweet steam.

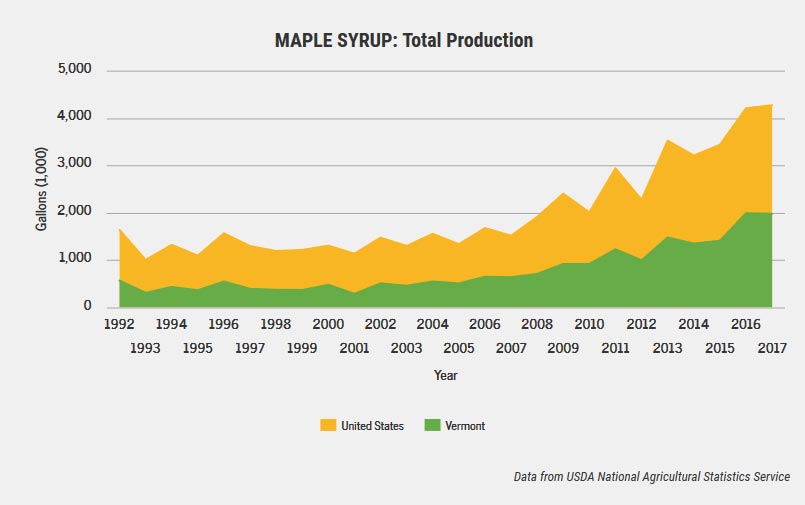

Since I don’t have much to report this time, let’s take a quick look at the business of sugaring as a whole – specifically the production explosion we’ve witnessed over the past decade. Below you’ll see two graphs, compiled by Mark Isselhardt, the University of Vermont Maple Extension Specialist, that seek to quantify the trend. If you look at the graph entitled Maple Syrup: Total Production, you’ll see that in 1994, the year Northern Woodlands was born, sugarmakers in the US were making around 1.3 million gallons of syrup. Last year they made almost 4.3 million. It should be noted that 80 percent of the world’s syrup is produced in Canada, and their industry’s growth has been on a similar trajectory.

In my observations, there are more small and mid-sized sugarmakers today than there have been in my lifetime, and technology has increased the amount of product we all make. But of course it’s the large operations that are really moving the needle. When I was a kid, 10,000 taps was a mega operation. Today, Sweet Tree in Island Pond has 500,000 taps, with plans for 1.5 million. Two hundred and fifty years ago schemers in the Northeast dreamed of a sugaring industry that would rival cane sugar – maple as a global commodity. There wasn’t the technology to accomplish this back then, but we’re on the brink of it now.

So where is this all going?

As of right now we’re still in the heady phase of the boom cycle. The marketers are doing their job and raising awareness of and interest in syrup throughout the country and worldwide. Demand has doubled in the past 10 years, according to a recent story in The Maple News, an industry trade publication, and this has led to opportunities across the board. An example of how this growth has positively affected our own small operation: We now have a market for sap right here in town that didn’t used to exist. If we can’t process everything we collect, we can sell the raw material to a big producer who’s hungry for it. Another local example: A sugarmaker up the road who makes about 3,500 gallons a year was telling me the other day that he’s selling his whole crop of syrup for a premium to a guy who’s aging it in whiskey barrels and selling maple bourbon syrup. Capitalism is creative, and the boom creates innovation and opportunity.

Of course raw capitalism is also destructive, destroying and then regenerating entire industries – it’s kind of like a disturbance-dependent ecosystem that way. And so booms are inevitably followed by busts. There are some cracks starting to appear in the maple bubble. Case in point is a funny headline in the aforementioned Maple News article that reads DEMAND THROUGH THE ROOF in all caps and in inch-high letters. And then below, a tiny subhead in lowercase letters reads: but bulk prices are dropping. The bulk buyer identified in the second paragraph who’s gushing about 10 percent industry growth is referred to as “one of the biggest buyers of bulk syrup in the country.” But by the end of the story, it’s revealed he’s not actually buying new bulk syrup. What’s happening here is that some big packing houses have essentially stopped buying from little guys. Instead, they’re locking in supply contracts with mega-producers, who produce all they need. Adopting cold, hard business logic, why would they buy in dribs and drabs from 1,000 producers – cutting 1,000 checks for an inconsistent product in an inconsistent and incoherent supply chain – when instead they can just cut one check to one mega-producer and have a clear chain of custody from forest to container? A buyer who is still buying from the little guys – Bruce Bascom in Alstead, New Hampshire – is paying around $2 a pound for table syrup, but says in the story that his stores are full enough that if it’s another good year prices are going to drop.

As a point of comparison, in 2008 the average bulk price for New England syrup was $3.72 a pound. We had a market for $4 a pound. So in 10 years it’s dropped in half. Obviously this is putting a lot of pressure on folks who expanded and took out loans based on these prices. It’s putting some pressure on family operations like ours that sell most of our syrup to boutique markets (country stores, farmstands, etc). While our wholesale prices have largely held, we’ve had a lot more competition lately and have had to really raise our marketing game. And I’m seeing stupidly underpriced syrup in other parts of the state as sugarmakers race each other to the bottom dumping their oversupply.

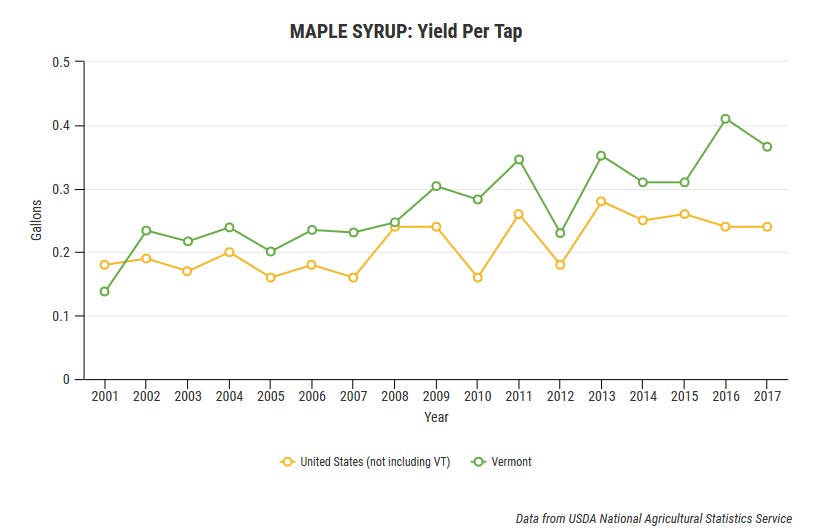

How can bulk prices drop by 50 percent in a decade and producers still be expanding? Because we’re farmers, yes, but the more statistically driven answer is because our yield per tap has gone up. If you look at the yield per tap graph above, you'll see that in 2007, Vermont sugarbushes were averaging under a quart of syrup per tap. Ten years later they’re over .4 gallons per tap. So we’re getting paid less but we’re making up for it in volume.

How long will that be sustainable? Dunno.

The growth of the mega-bush is leading to some interesting debates in conservation circles. Consider the case of a new 200,000-tap operation that’s going in on land in northern Vermont that’s subject to a conservation easement. Sugaring is a permitted use, along with forestry and public recreation. But is the 40,000 square foot sugarhouse complex that’s being built on-site really a sugarhouse? Or is it a factory that makes syrup? And if so, does a factory in the woods fit the spirit of the conservation easement? What about the three-phase power that’s being run out into this undeveloped area, since development usually follows where you run power? Do hikers, hunters, snowmobilers, and others who recreate on the land have a right to object to 4,000 acres being strung with millions of feet of plastic sapline that will stay up year-round?

These are questions that few people saw coming 10 years ago.

Discussion *