Anyone who reads the papers knows how badly the prices of stocks, houses, and mutual funds have done since the market peaks of a few years ago. If you don’t sell stumpage very often, you may have been spared seeing how timber prices have also declined. But you’ve probably noticed, through home improvement projects and visits to the furniture store, that how we buy and use wood has changed. Combined with the recession, this has changed the value of the timber on your back forty – and not for the better.

The volume of wood being purchased is down, operating mills are down, loggers are being forced to work less, and stumpage values (the prices paid to landowners for standing timber) are lower. Nationally, from 2005 to 2009, softwood lumber production fell by roughly one-half. Hardwood lumber production fell by a bit more. In such a market, it’s a wonder that stumpage values in the Northeast did not disappear entirely.

Several colleagues and I recently analyzed stumpage prices in Maine over the past half-century, using data gathered by the Maine Forest Service from 1959 to 2009. Now, most of you do not own land in Maine, but these trends can yield insights that apply to forestland across the Northeast. The lessons we learn from looking back can help us be more realistic about our future goals and expectations.

Focus on Moving Up

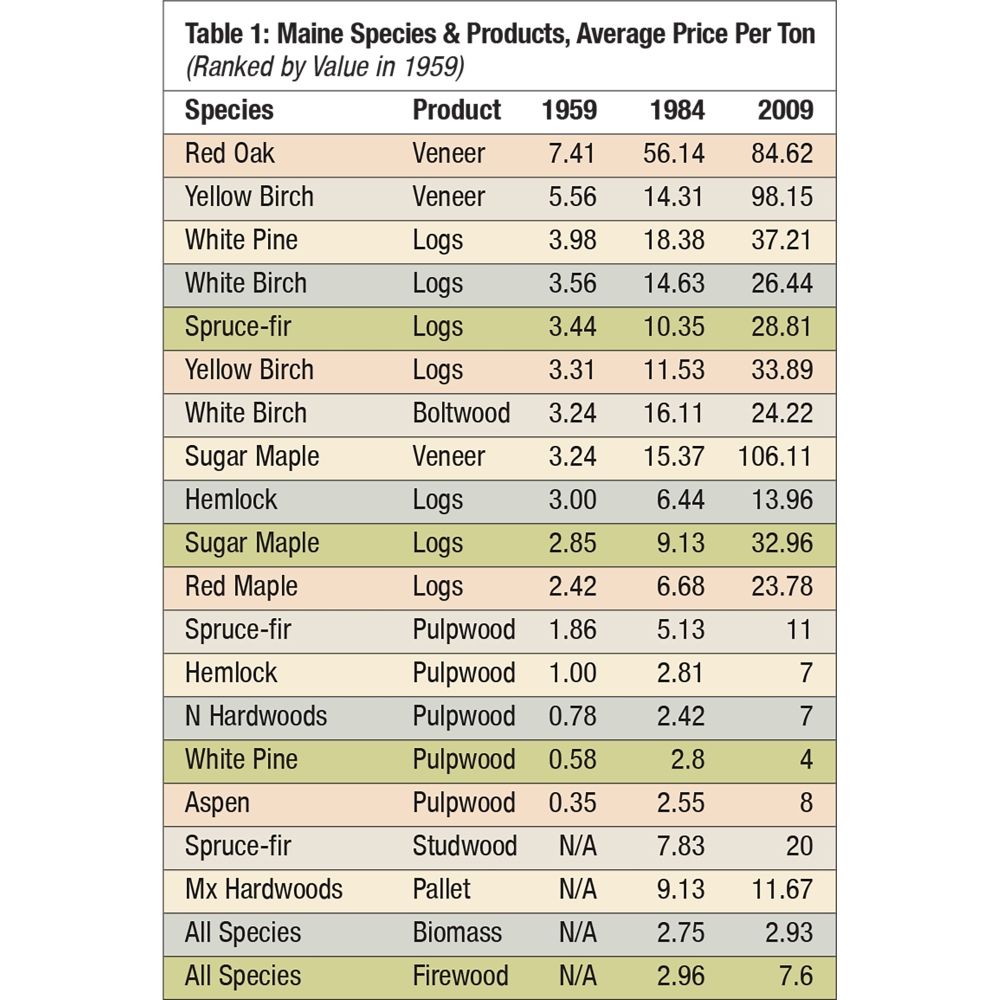

Our survey of stumpage data produced an array of tables, statistics, and charts that only a policy wonk could love. One way to reduce the data to a straightforward picture is to simply rank species and products by their value per ton (Table 1), shown here at three points in the past half century.

Notice that large differences between species and product classes persist over long periods of time. Although some items change in rank over the decades, the ones that were worth the most in 1959 are still among the most valuable in 2009.

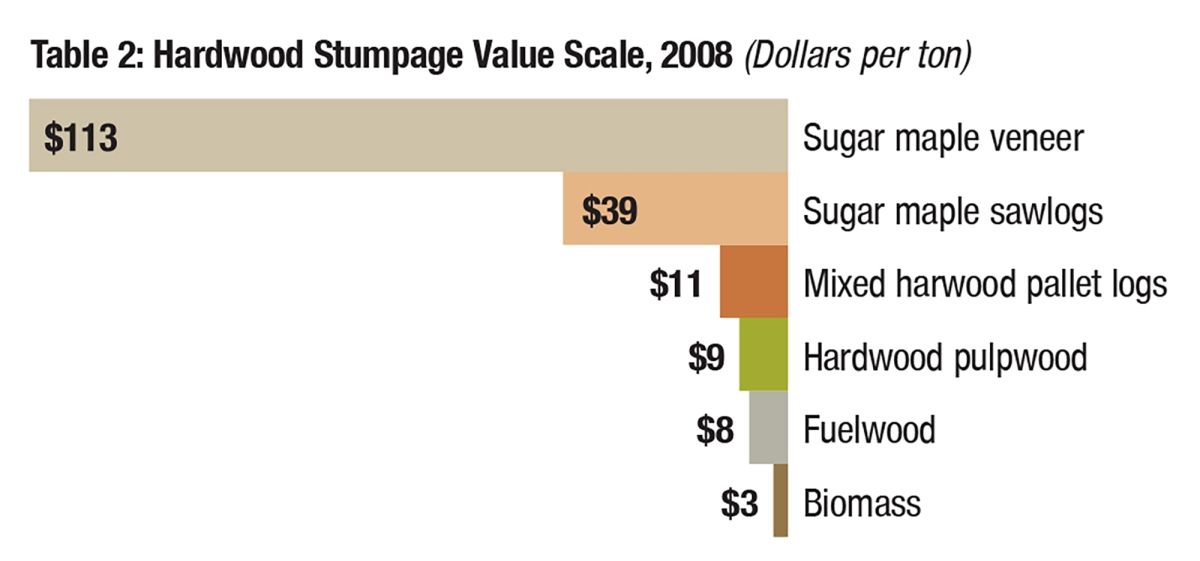

Let’s take sugar maple as an example (Table 2). The differences between the log and veneer product classes are very large; the differences between the firewood and pulpwood/biomass are smaller. On the surface, this illustrates the obvious fact that veneer is the most valuable product class. But from the perspective of an investor, the product class isn’t important, the rate of return is. If a sugar maple can improve in product class from, say, biomass at 4 inches diameter at breast height (dbh) to firewood at 6 inches, then it could increase in value by 6.8% per year in 15 years. We all wish we had more logs and veneer, but many of us are managing woodlots that have been sloppily cut for generations and are heavy on firewood and light on veneer logs. The take-home message is that if you can identify a tree with potential to gain a product class in the coming cut cycle, it ought to be retained. A tree with no upgrade potential can be considered for removal. This applies to both high-value and low-value items. Make your management plan for one cutting cycle at a time. The future will take care of itself if you make sound decisions now.

Don’t Sit on Your Woodlot, Manage It

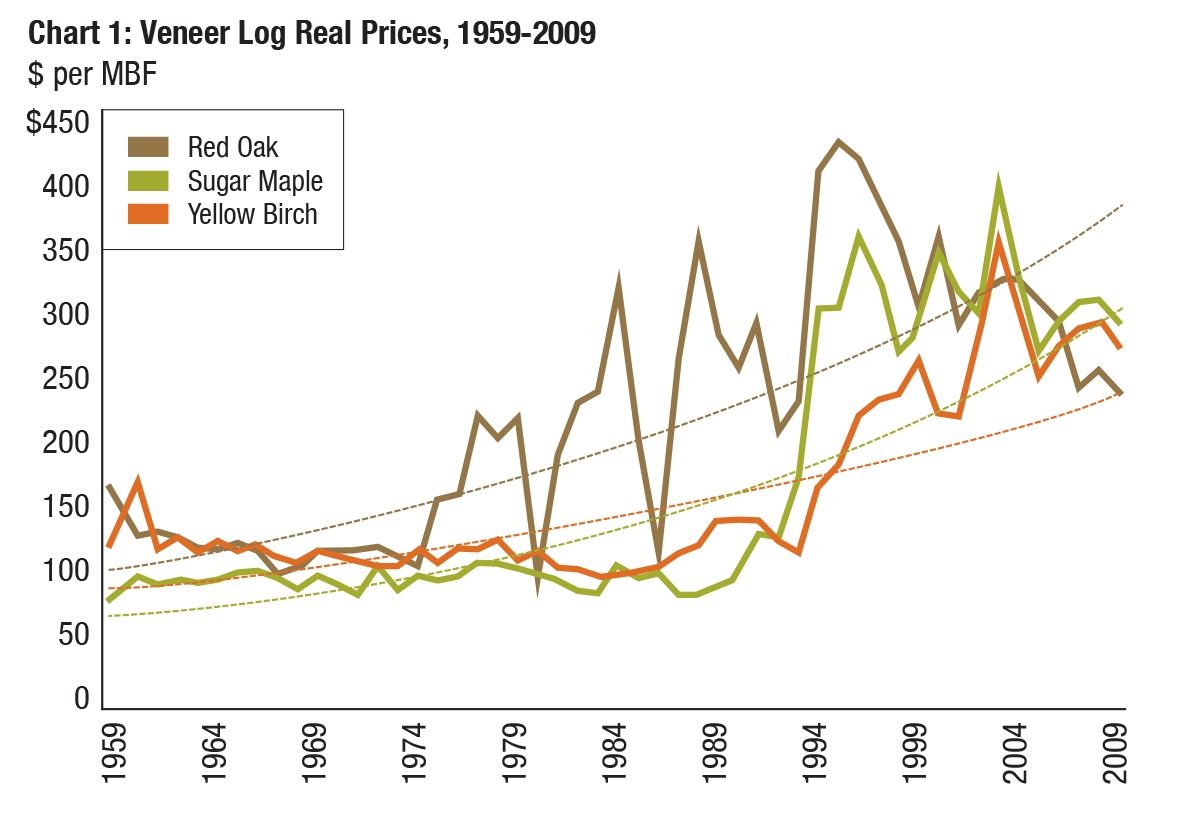

As we tease the data further, other interesting trends appear. One tempting notion is to time the market and cut your wood when prices are good. This is an understandable impulse, but the graphs illustrate how hard this can be. Take red oak as a prime example (Chart 1).

Had you been the owner of oak in 1983 and said, “Prices are high, time to cut!” you would have kicked yourself for not waiting another 20 years. Conversely, had you been considering cutting in 1994-96 and opted to wait another cutting cycle, you would have lost substantial value in the subsequent washout.

Rather than trying to be a fortune teller, it may be easier to just notice when prices are unusually low and defer cutting during such periods. Instead of trying to predict peaks for cutting high value trees, you should watch for unexpected peaks in market demand and use them to get the marginal jobs done – thinning or removing species that in ordinary markets can’t be sold.

In the financial world, dollar-cost averaging is an old investment strategy. An investor buys a certain amount of stock every month or quarter, regardless of the level of the market, in order to avoid mis-timing the market. A similar notion applies to planning timber harvests. You should plan for frequent light harvests rather than infrequent heavy ones. Not only will operating frequently enable you to pick up on silvicultural opportunities, it will also help you avoid mistiming the market. You won’t sell a lot of wood at the highest prices, but you also won’t miss those prices completely. Frequent light harvests also enable you to fund taxes and regular expenses out of current income. Periodic income boosts the total returns on the asset, whether you reinvest it in the woodlot or in something else.

Holding timber without doing any management barely beat inflation from 1959-2009, based on the average of the items in the table. Consumer Price Index inflation was 4.1%, and the average wood product listed increased 4.7%. The typical woodlot probably fell behind inflation because its value was concentrated in low-valued items. Another take-home message: Investment results come from management, not from sitting around and waiting.

Wood as a Fashion Item

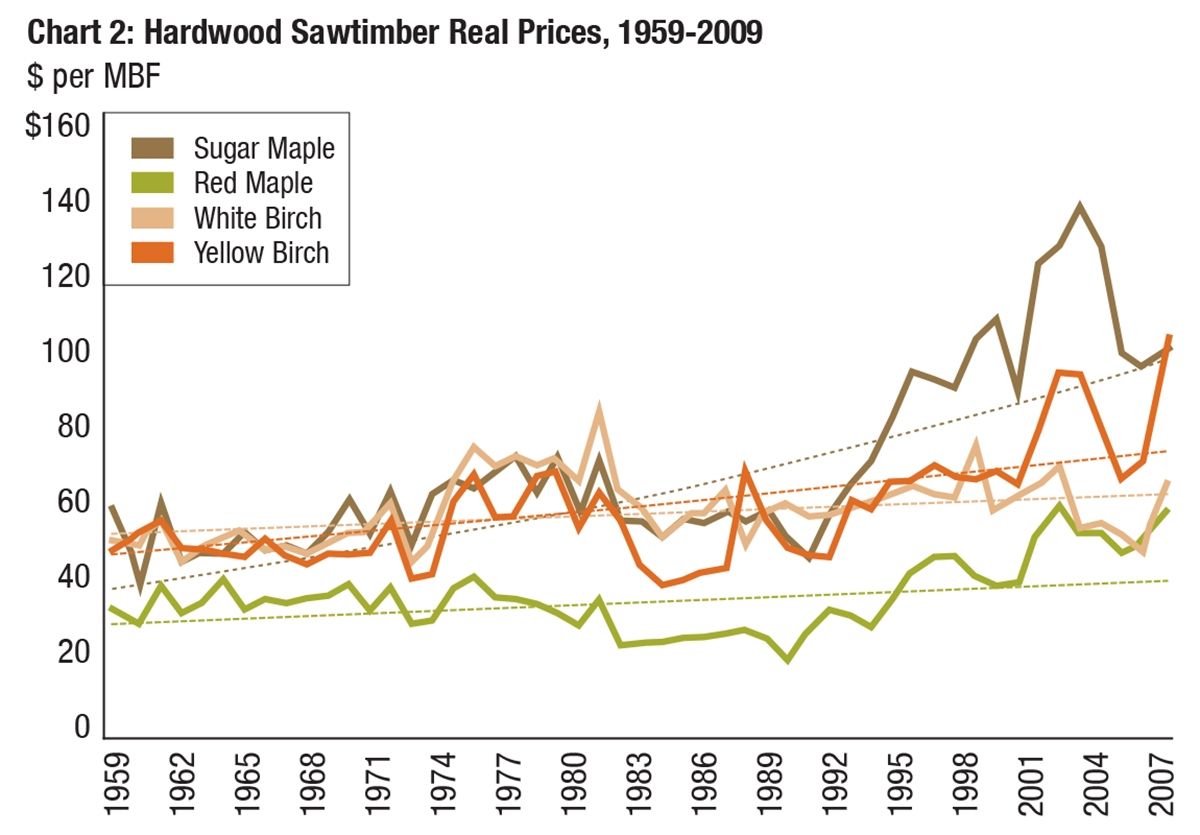

Another valuable lesson the past provides is that wood fashions come and go, and market conditions may be very different in 20, 40, or 50 years. Look at the white birch line on the Hardwood sawtimber chart (Chart 2).

In the late 1970s, white birch boltwood was one of Maine’s most valuable woods. It was used for Maine’s famous toothpicks, turnery items, dowels, and many other things. Small birch-turning plants dotted the northern New England landscape. But then people found that ramin, a tropical tree species in the genus Gonystylus, could be used to make dowels more cheaply. (In a sad twist, ramin is now considered threatened in at least part of its range.) Birch from Mongolia was also found suitable for turning. The final blow came when the plastics industry took over the production of specialty products, like golf tees and coffee stirrers. Within 25 years, the dowel plants were almost gone, and since the mid- 1980s, the real value of white birch has fallen. The red maple trend line also reflects changing wood fashion. Red maple prices were barely worth tallying when they initiated the price report in 1959. Red maple stumpage rose significantly after the late 80s, though, reaching the level of white birch.

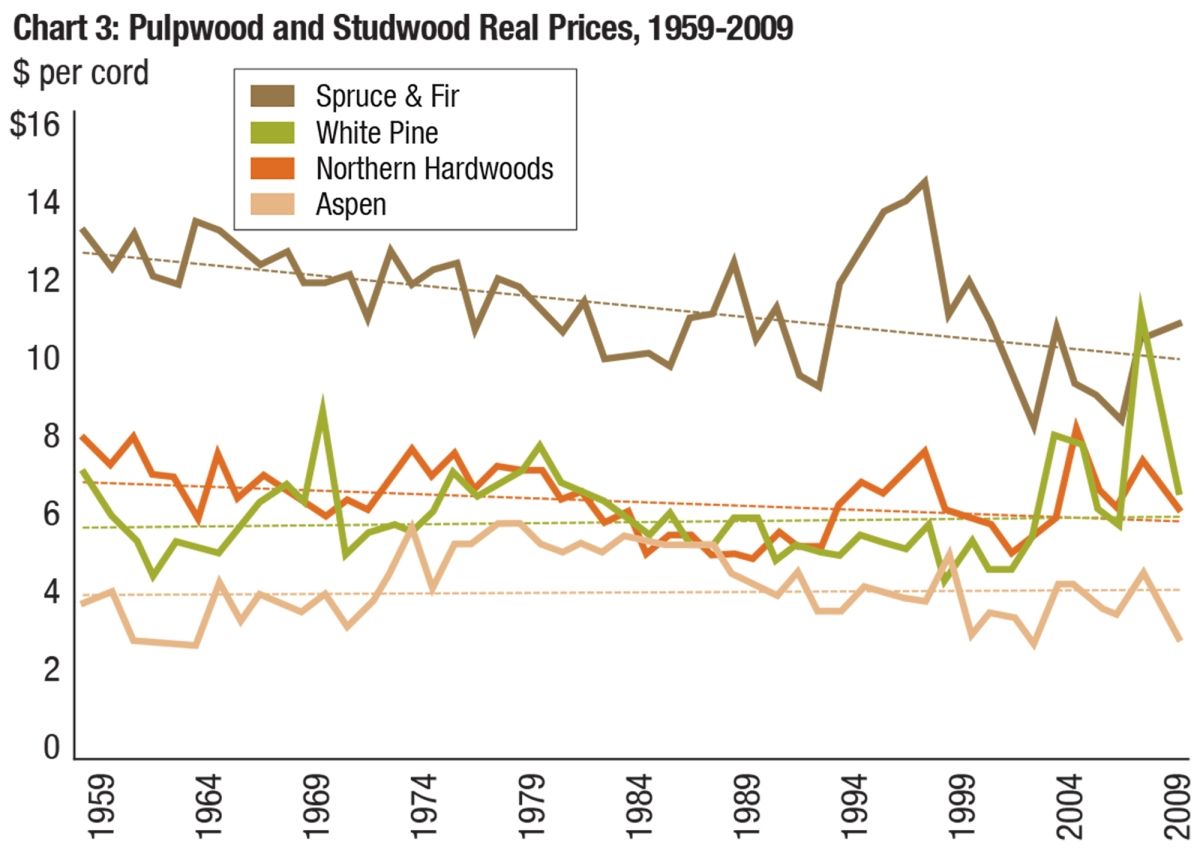

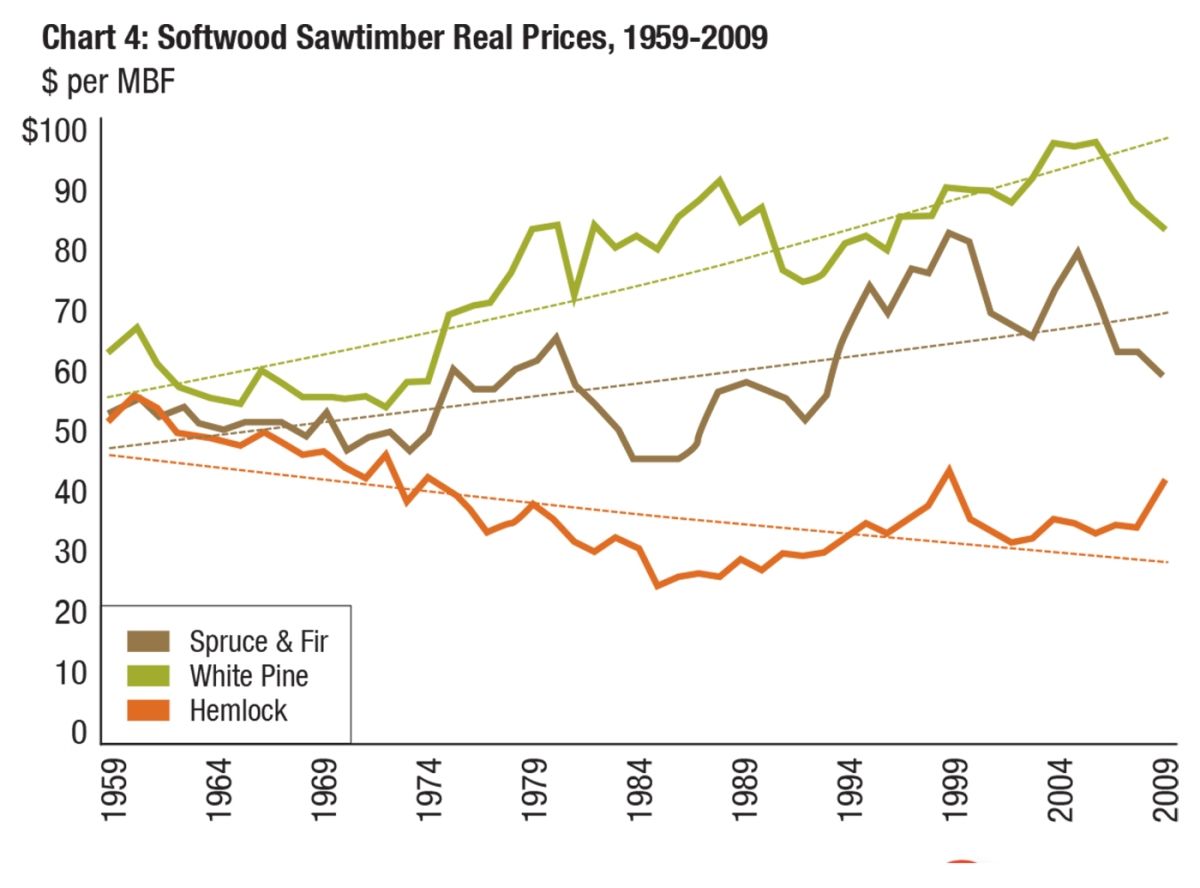

When we study the Maine pulpwood and studwood (small sawlogs used by specialized mills) stumpage price graph (Chart 3), we see a market in decline. Spruce and fir have always been the premier pulpwood species in the Northeast. Yet their prices fell consistently from 1961 to the early 1980s. Prices rose briefly in the 90s, then faded, leaving prices below the long-term trend line by 2006. White pine has been a valuable species, in good grade logs, for generations (Chart 4).

Yet, pine lumber prices began falling well before the 2005-2006 housing peak, due to competition from imports and nonwood substitutes. The odds that pine can recover all of those lost markets are remote, though.

Will the Markets Bounce Back?

Experience shows that I am a poor forecaster. Like many others, I underestimated how severe the current market downturn would be. The restructuring in the region’s wood industry, though, is not just a downcycle after which all will return to normal. It has driven out many mills, small and large, and few of them will ever reopen. Worse, do you know any young people who want to go into manufacturing – especially in wood products? I don’t. So, who will pick up the pieces when markets rebound?

Most people accept that the 1999-2005 peaks in securities markets, housing construction, and wood products were not normal – they represented an unsustainable bubble. A return to those levels will be long in coming. Supply constraints are likely to be tight in most places, though, which could lead to a rise in stumpage prices as the economy begins to recover. But I wouldn’t make any decisions premised on rapid increases in stumpage prices in the coming five years.

Conclusion

Analysts (like this author) like to torture readers with graphs and statistical procedures of one kind or another. But the bottom line is quite simple: Maintain diversity in your woodlot. Use market booms to get marginal jobs done. When possible, mark your stands to upgrade stems to the next product class. Think total return and not just annual price changes. Don’t try to time the market; instead, cut lightly and frequently.

When managing for any of the higher value-wood products, a low-grade wood market is critically important. When the demand for solid wood products is in a down cycle, it’s crucial that a landowner be able to sell smaller, lower grade, and minor wood species. If you can net just $2.00/ton for biomass, it can add $20-$40 per acre to harvest revenues. This won’t buy a ticket to Florida, but it will help pay the taxes. It will enable you to complete thinning and stand-improvement projects.

Without low-grade wood markets, it becomes tempting (or downright necessary) for landowners to cut only the best timber on their woodlots. Instead of improving the forest, this depletes its value. In the long run, this may deplete the genetic stock of the forest; it certainly hurts the future of the wood-products industry, and it reduces the economic value of the forest property.

Discussion *